What happened in the markets last month

The month started with a broad sell-off in risk assets after Donald Trump announced 25% tariffs on Canada and Mexico, 10% on China and ramped up his threats against the European Union. Shortly thereafter, though, he had agreed to postpone tariffs on Canada and Mexico for 30 days, which helped stocks recover, and many indices hit new all-time highs. The narrative took another turn at the end of the month, when Trump confirmed that previously announced tariffs would come into force, including 25% tariffs on the EU. This led to a global selloff in equities and CNN’s Fear Greed indicator flashed ‘extreme fear’ at the end of the month. Economic data in the US was overall weak, while inflation rebounded, sparking stagflation fears, but Federal Reserve Chair Powell signalled patience before cutting interest rates further. US pending home sales, for example, have fallen to a new all-time low, worse than during the pandemic, and worse than in 2008. ‘Real-time inflation’ dropped sharply to 1.5%, according to Truflation.

Many European indices reached record highs, driven by optimism over Ukraine peace prospects. France’s Prime Minister Bayrou passed a budget, and the Bank of England cut interest rates, while at the same time lowering its growth forecast. In contrast to the US, economic data mostly surprised to the upside. On the last day of the month, talks between Ukraine’s president Zelensky and the US president collapsed after the pair's meeting at the Oval Office descended into a shouting match.

The German DAX index hit an all-time high after Friedrich Merz, the leader of the CDU/CSU party, won the federal election with 28.5% of the votes and now plans to form a coalition with the SPD party by Easter. The election saw high voter turnout, with younger voters favouring the extreme left and extreme right parties. Merz’s agenda includes tax cuts and increased spending, in particular for defense, but the economic outlook remains difficult with bankruptcies at a 10-year high.

China weighed retaliation after Trump’s tariff threats, and Chinese technology shares jumped as the emergence of DeepSeek sparked optimism over the country’s competitiveness.

Gold reached new record highs, while the crypto market experienced a historic sell-off.

What happened in the fund in the last month

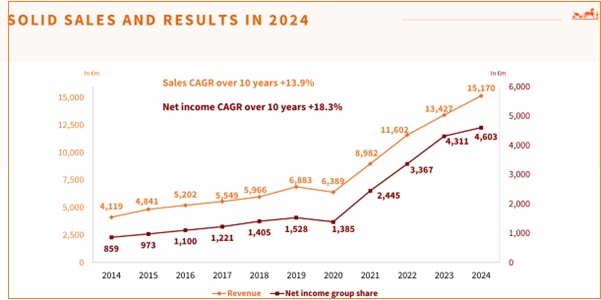

Sentiment in the financial community for the luxury sector had been very poor, mainly due to an ongoing muted economic environment in China. And while LVMH’s results, reported in January, were rather underwhelming, Hermes managed to surprise the market with strong results. Revenues rose by 18% in the last quarter of the year, and sales of leather goods were even up 22%. Both in Americas and in Europe (ex France), sales increased by 21%. The year started well for Hermes, although due to last year’s stellar performance, the comparison base for 2025 is of course getting more difficult. As can be seen in the chart below, the company’s long-term track record is amazing, and even more so as the number of stores worldwide has decreased since 2014 from 314 to slightly less than 300 today.

Source: Hermes

Ferrari reported solid results as well. In 2023, the company shipped 13663 cars, and with 13752 in 2024, this number increased by only 0.7%. Mainly thanks to personalizations, this led to an increase of earnings per share of nearly 23%. Ahead of the results, there was speculation that demand for the new supercar F80 may be disappointing, but this has been categorically denied, and all of the 799 models have been allocated. The new electric model will be presented in October, and most importantly, the order book covers all of 2026. Interesting to note is that 81% of the Ferrari buyers in 2024 were existing clients, and 40% own more than one Ferrari.

Outlook

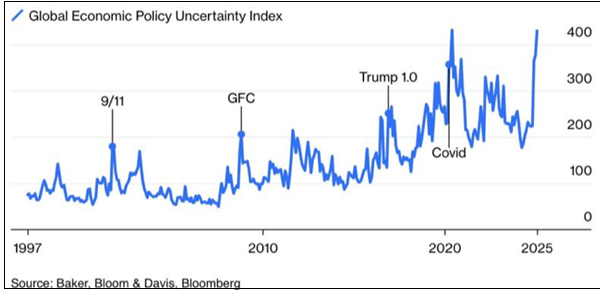

Volatility in global markets increased sharply, and many of last year’s winners are this year’s losers. This level of uncertainty and nervousness can best be seen in the below chart, which shows that the Global Economic Policy Uncertainty Index is near its highest levels ever!

Global financial markets are extremely volatile, and ‘played’ the threat of huge tariffs one day, and then took the opposite position shortly thereafter on news that tariffs were postponed. Another topic the market was ‘playing’ was a potential ceasefire in Ukraine. The word ‘playing’ describes best this market action, which is the exact opposite to our investment approach. We aim to identify, and buy, and hold, good companies. This includes filtering out the daily news, which can often be regarded as ‘noise’. Companies we invest in have to have a good track record of continuous growth of both sales and earnings, as this is usually proof of a superior business model with a good market share and decent pricing power. We don’t like debt in general, as this may cause problems when times get tough, and on the other hand, with net cash on the balance sheet, companies can be opportunistic and seize opportunities at any moment in time, no matter how high interest rates are or how depressed the economic environment is. But it has to be kept in mind that when investing in companies over a long period of time, there will be more difficult environments for various reasons, and no company will successfully manage to report outstanding results all of the time. And more crucially, there are always periods when the market wants to play certain themes, like for example a ceasefire in Ukraine or a tariff war.

There are always periods when even the most reasonable investment strategies underperform

This means that there are always periods when even the most reasonable investment strategies underperform. In these difficult time periods it is crucial, in our view, to believe in the strategy, and even more importantly, believe in the companies we own, as they have achieved overall great success over the last years. And as long as there are realistic prospects that the past success will be continued in the future, we stick with our holdings, and don’t try to run after the latest ‘trend’ investments. Very simply put, will the world need more chips in the future at a time when Artificial Intelligence applications make their way into everybody’s daily lives, which leads to a further, sharp increase in data being generated, and being analysed (to sell more products)? Will there be more wealthy people around the world, who want to use make-up and perfume or treat themselves to a beautifully crafted handbag, or an amazingly designed, rare sports care? We think the answer to these questions is yes, and hence we will continue to own great companies, even if ‘Mr Market’ sometimes prefers other sectors, and other strategies. Over the long term, share prices follow earnings, and time in the markets beats timing the markets. At the time of writing, the companies we own are expected to increase their earnings per share by more than 15% this year compared to last year, and another 12% in 2026, and are at the same time valued nearly 20% below the average valuation of the last 10 years.

Written on 13 March 2025

On the day of writing this article, MW GESTION ACTIONS EUROPE holds the following quoted securities: :

Ferrari for 6.2% of its outstandings

Hermes for3.7% of its outstandings

LVMH for 3.1% of its outstandings

Communication-Marketing

The MW Actions Europe fund is a compartment of the Luxembourg SICAV MW ASSET MANAGEMENT. You should contact the fund management company MW GESTION or your financial advisor for more information.

Past performance is not a reliable indication of future performance. Past performance is no guarantee of future performance.

The content does not constitute a recommendation, an offer to buy, a proposal to sell or an invitation to invest.

Further information is available on the company's website: www.mwgestion.com, in French, English and Italian..