What happened in the markets last month

The month began with solid labour market and inflation data in the U.S., before markets were lifted by news of a trade deal between the U.S. and China. Alongside positive commentary about trade negotiations with several other countries, the global trade policy uncertainty index fell further from the all-time highs reached in April.

Volatility spiked when tensions between Israel and Iran escalated, and oil prices surged as the U.S. became involved. However, nearly all of these gains reversed after Donald Trump announced a ceasefire, and the VIX volatility index dropped to levels not seen since February.

Overall, U.S. economic data was rather disappointing. Housing starts, for example, fell to their lowest level in five years, and continuing jobless claims reached their highest point since November 2021. This triggered renewed criticism of Fed Chair Jerome Powell by Donald Trump, and the U.S. dollar fell to its lowest level since 2022. Nevertheless, by month-end, several U.S. indices reached new all-time highs, partly fueled by renewed optimism around Artificial Intelligence.

European markets underperformed, despite signs of economic improvement. The euro area’s manufacturing Purchasing Managers’ Index hit a 33-month high in May, while Germany’s IFO and ZEW sentiment indicators came in above expectations. Germany’s tax break package was approved, and NATO allies agreed to increase defense and related spending to 5% of GDP by 2035. Both the European Central Bank and the Swiss National Bank cut interest rates again.

However, the Bank of France revised its growth and inflation forecasts downward through 2027, citing the impact of U.S. tariffs on European economic activity. Despite this, both the EU and U.S. remain confident that a tariff agreement can be reached by the July deadline.

What happened in the fund in the last months

The first half of the year was marked by high volatility. European markets began strongly, supported by optimism around economic recovery, fueled in part by increasing infrastructure and defense spending programs. However, this positive sentiment reversed abruptly when Donald Trump unsettled markets with new tariff threats, triggering a sharp correction in global equities.

As a result, global trade policy uncertainty reached record highs, weighing particularly on internationally exposed companies. In contrast, firms with more domestic or regional operations outperformed. This environment negatively impacted our portfolio, as many of our holdings operate globally. Sectors such as luxury goods and semiconductors—traditionally beneficiaries of globalization—suffered disproportionately.

Fears that trade tensions would lead to collapsing future sales and earnings caused a widespread sell-off among our holdings. At the beginning of April, analysts had forecast earnings growth of around 15% for our portfolio companies. However, valuations dropped sharply: the forward price-to-earnings (P/E) ratio fell below 20, which was nearly 30% below the 10-year average for our holdings. This reflected significant investor panic and uncertainty around future growth.

Despite this, the sell-off was short-lived. Markets recovered quickly, and while tariff negotiations are ongoing, earnings expectations for our companies remain stable or have even improved slightly. For example, 2025 earnings are now expected to grow by 16%. Although valuations have rebounded, our portfolio still trades at a roughly 10% discount to its 10-year average—while the Euro Stoxx 50 Index trades 9% above its own long-term average.

Top Contributors:

The strongest performer in the first half was Gaztransport & Technigaz (GTT), a specialist in containment systems for the shipping and storage of liquefied natural gas (LNG). With a near-monopoly in its niche and a positive long-term outlook for LNG, the company’s order backlog is well secured until the second half of 2028—offering welcome visibility in a volatile environment.

Deutsche Börse was the second-best performer. In addition to its structural growth drivers, cyclical factors such as increased trading volumes across asset classes benefitted from the spike in market volatility during the correction.

Detractors:

On the negative side, LVMH underperformed significantly. The deteriorating environment for luxury goods, driven by tariff-related uncertainty and weakening consumer sentiment—especially in China—has hurt demand. Sales declined in Q1, and pressure on margins may increase if higher tariffs cannot be passed on to consumers. We have therefore reduced our position in recent months.

Novo Nordisk also disappointed, extending last year’s decline after clinical data for a potential blockbuster drug failed to meet expectations. Recent quarterly results fell short of forecasts, and long-serving CEO Lars Fruergaard Jørgensen stepped down. While the obesity market remains dynamic, Novo Nordisk must now work to regain lost market share—particularly in the U.S. Additionally, the weaker U.S. dollar negatively impacted both Novo Nordisk and LVMH due to their significant U.S. operations.

Outlook

Newsflow—and, with it, sentiment in global markets—has improved markedly in recent weeks. This shift is perhaps best reflected in CNN’s Fear and Greed Index, which has returned to the “extreme greed” zone after spending more than two consecutive months in “fear” or “extreme fear” territory. Another key sentiment gauge, the VIX volatility index, has also eased, falling back below 20 after having spiked above 50 in April.

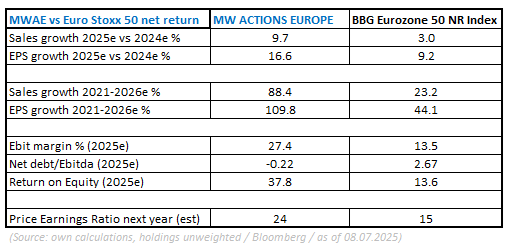

As shown in the table below, the characteristics of the fund have remained unchanged. In our view, maintaining a consistent investment strategy—particularly during periods of heightened uncertainty—is essential to long-term success.

And these are indeed challenging times. In Europe, traditionally defensive sectors such as Banks, Construction, Utilities, and Telecommunications have outperformed so far this year, while typical growth sectors—such as Consumer Products, Healthcare, and Technology—have significantly underperformed.

As a result, European growth stocks are now trading at their lowest relative level compared to the broader European market in over six years. In our view, this makes their valuations particularly attractive from a historical perspective.

Written on 10 July 2025

On the day of writing this article, MW GESTION ACTIONS EUROPE holds the following quoted securities: :

- Deutsche Boerse for4.5% of its outsandings

- GTT 3.6 % of its outstandings

- LVMH for 0.6% of its outstandings

- Novo Nordisk for 2.7% of its outstandings

Communication-Marketing

The MW Actions Europe fund is a compartment of the Luxembourg SICAV MW ASSET MANAGEMENT. You should contact the fund management company MW GESTION or your financial advisor for more information.

Past performance is not a reliable indication of future performance. Past performance is no guarantee of future performance.

The content does not constitute a recommendation, an offer to buy, a proposal to sell or an invitation to invest.

Further information is available on the company's website: www.mwgestion.com, in French, English and Italian.